Hitachi recently introduced fi ve new electric-powered, mining-class excavators that, except for the

Hitachi recently introduced fi ve new electric-powered, mining-class excavators that, except for the

absence of

diesel engines and their ancillary systems such as fuel tanks, muffl ers, etc., are functionally

identical to the companys

popular diesel-powered versions such as the EX8000-6 shovel shown here.

Trucks, shovels and large wheel loaders

have long been mainstays of primary production

in most types of surface mining,

and both OEM and aftermarket suppliers

can point to decades of giving their customers

what theyve asked forhigher

truck-body and bucket payloads, lower

cost of operation, improved operator safety

and moreas a principal driving force

that has kept truck/shovel mining at the

forefront of the industrys technological

interest for so long.

In good times, miners ask for a lot

they love the big trucks, shovels, and

loaders that allow them to operate fl exibly

and move more dirt, with less people

in the pit and fewer trucks on the

haul roads, so when reports emerge from

equipment auctions in Australia, where

late-model wheel loaders that originally

cost almost $3 million are being sold for

high-fi ve-fi gure bids; or from South America,

where the worlds largest Caterpillar

dealer reported that only one mine in that

highly active mining region had submitted

a public tender for ultra-class haulage

trucks (four) in the entire year of 2015,

it effectively illustrates the depth of the

industrys slump.

In bad times, miners ask for lessa

lot less. In fact, industry spending on

big-ticket mobile surface equipment

has been in a downward spiral for more

than four years, dropping to a level in

early 2016 that is about 75% less than

the industrys most recent spending

peak in early 2012. The Parker Bay Co.,

a U.S.-based market research fi rm specializing

in global surface-mining equipment

sales and trends, recently released

a market analysis for sales of high-capacity

trucks, shovels and loaders (see sidebar)

that explores this drop-off, noting

that its results indicate large surface

mining equipment shipments

are now

at levels not seen since the start of the

commodities Super Cyclerepresenting

a 10-year low.

Smaller Equipment Strength in Numbers

Although its apparent that mine operators

have hit the brakes on large-equipment

purchases, Parker Bay noted in a

recent bulletin that theres a tiny ray of

light inside the long, dark fl eet-acquisition

tunnelalthough the total value of

mine mobile equipment deliveries declined

in the fourth quarter of 2015, the

actual number of units shipped increased

by 6% over the previous quarter.

The higher number of equipment units

shipped, however, is attributed to purchases

of smaller trucks and dozers; mine

operators just arent spending money on

ultra-class trucks, massive rope shovels

or high-capacity excavators at this time,

but high-grade/low-tonnage specialized

operations in Africa, Asia and elsewhere

are buying signifi cant quantities of smaller

equipment that more closely suits their

needs. Volvo Construction Equipments

Terex Trucks division, for example, just

delivered 29 Terex haulers19 TR100s,

rated at 100-ton capacity, and 10 TR60s,

capable of carrying 60-ton payloadsto

a jade-mining operation in Myanmar. A

coal mine in Bosnia purchased nine Terex

TA300 articulated trucks to haul 30-ton

payloads out of the pit.

In an example that underscores the

focus on meeting specifi c, affordable

needs forced upon operators by current

economic conditions, a large phosphate

producer in Morocco found an alternative

to buying large, conventional service

trucks to maintain its fl eet of 22 rigid-

body haulers, along with large wheel

loaders, two dozen bulldozers, six drill

rigs and several water tankersit converted

two Volvo CE A30F articulated haulers

into customized service vehicles that can

effi ciently negotiate the rough terrain at

the producers mines.

Scania, another global truck builder

with a large presence in the over-the-road market, also has market share in

the smaller-hauler end of the mine truck

market, offering three, four and fi ve-axle

dump trucks with up to 46-mt payloads

most of which are available in AWD confi

gurations that enable their use for both

in-pit and outbound road haulage.

Scania has been researching and developing

driverless truck concepts for

some time, and reports that testing of its

haulers in real-world site conditions is not

far off. Scanias customers in Australia

are already discussing potential application

opportunities for the future, with

mining very near the top of the list.

Inside the cab of Hitachis new electric-powered excavators, fl uid-fi lled elastic mounts reduce

Inside the cab of Hitachis new electric-powered excavators, fl uid-fi lled elastic mounts reduce

shock and vibration

by up to 30%, and an advanced multidisplay monitor provides key machine

status information.

Currently, prototypes are being used

to test the capabilities of Scanias remote-

control technology. Scania said its

Astator test vehicles have been developed

to the point where they can now

function without a driver in the seat on a

test track, running through simulations of

loading and unloading under remote control.

Theyre also capable of safely dealing

with obstacles on the road.

Developers at Scania and researchers

from technical colleges in Sweden are examining

the role driverless trucks could

play in future mining scenarios. Mines

are environments that are especially well

suited to self-driving vehicles, said Lars

Hjorth, in charge of predevelopment within

Autonomous Transport Solutions at

Scania. The area is contained and the

operator can control what equipment or

personnel are working in the area.

The company noted that interest is

increasing around the world in smaller

and more fl exible solutions involving specialized

mining trucks. A truck solution

is more cost effective, with the total cost

per transported ton being significantly

lower, said Hjorth. The infrastructure

costs are also reduced as trucks dont require

specially reinforced roads.

In Australia, Scania said it is already

talking with a number of customers regarding

potential applications for driverless

trucks, for both off-road environments

and on-road usage. We see a lot of

opportunity for Scania to leverage its autonomous

truck technology in the not-sodistant

future in Australia, said Robert

Taylor, general manager of Scania Australias

Mining and Resources division.

Customers are already talking with us

to fi nd out how we can assist them to implement this technology for specifi c applications.

There is also a lot of interest

in platooning for road train line-haul work

as well, he noted.

Expanding the Lineup

Despite the slump in equipment purchases,

suppliers havent abandoned

product-line expansion and upgrade programs.

Last November, for example, Caterpillar

introduced its 6015B diesel-powered

excavator, featuring bucket capacity

sized to cater specifi cally to applications

in small mines, quarries and large earthmoving

projects.

Swedish truck builder Scania is testing prototypes of its all-wheel-drive, in-pit/over-the-road haulers with

Swedish truck builder Scania is testing prototypes of its all-wheel-drive, in-pit/over-the-road haulers with

driverless

operation, and reports strong interest from Australian mining customers.

In February of this year, Hitachi

Construction Machinery Americas introduced

fi ve electric mining shovelsthe

EX1900E-6, EX2600E-6, EX3600E-6,

EX5600E-6 and EX8000E-6. Bucket capacities

for the new models range from

11 m3 (14 yd3) for the smallest model

to 40 m3 (52 yd3) for the top-of-the-line

EX8000E-6.

Brian Mace, manager of HCMs mining

applications group, told E&MJ that Hitachi

has offered electric excavators as part

of its product line since the mid-90s, but

the new models are confi gured specifi cally

for the U.S. and Latin American markets,

where electrical power is provided at

60 Hz rather than the 50-Hz frequency

common in other parts of the world. Because

Canada and Australia impose a particular

set of electrical power safety standards

on this type of equipment, Hitachi

is not quite ready to offer the new series

in confi gurations eligible for use in those

countries.

The electric-powered series are identical

in most respects to Hitachis EX-6

series diesel-powered excavatorsexcept,

of course, for the absence of the

diesel engine, fuel tanks and air-fi ltration/

muffl er systems, which results in

the electrical models having an operating

weight savings ranging up to 37 tons

in the largest model, along with a corresponding

lower ground pressure. The

space normally taken up by the diesel

models fuel tanks is used to house the

electrical control cabinets in the electric

models. The electric shovels also are

equipped with a slip ring in the center

joint to transmit power to the motor(s).

Although the power-handling components

on the electric machines are designed

to work with either 50- or 60-Hz power,

the mechanical gear ratios on the electric

versions must be changed to maintain

constant hydraulic pump speed at

either frequency.

The fi ve new electric models feature

advanced Hitachi TFOA-KK motors designed

to provide a cost-effective alternative

to diesel-powered machines for

mining operations where suitable electric

power is available. Motor voltage ranges

from 6,600 VAC to 6,900 VAC, providing

continuous output rated at 610 kW on the

EX1900E-6, up to 1,200 kW x 2 on the

EX8000E-6.

Mace pointed out that a mine operators

specifi c site or project characteristics

can have a major infl uence on which

type of machine would be more effective.

Greenfi eld mine projects for which a reliable

electrical power supply is not yet

available would likely not be a good match

for electric excavators, while an operation

that must comply with local noise or exhaust-

emission restrictions could benefit

significantly from their use.

The need for a trailing power cable

might put an electric model at a disadvantage

vs. a diesel-powered unit at an

operation that requires the highest level

of mobile fl exibility from its excavators.

On the other hand, electric shovels models

simplify daily maintenancethe machines

do not require consumables such

as engine oil, fi lters, coolant or fan belts.

Engine-related components are also eliminated,

such as radiators, air filters and

muffl ers. Service life of certain components

may be extended due to the elimination

of engine-generated heat.

As is the case with the diesel versions,

the E-6 series electric drive excavator

front attachments use welded, low-stress,

high-tensile-strength steel for a full box

section design that resists twisting and

bending forces. The undercarriage for

the fi ve new models is identical to the

diesel machines.

Looking Down the Road

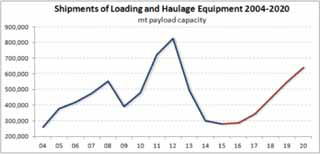

Parker Bays Market Analysis and Forecast: Loading and Haulage

Equipment, released in early March, reported a 10-year low

for large surface mining equipment shipments, which are now at

levels not seen since the start of the commodities Super Cycle.

With the current downturn approaching the end of its fourth

year, the companys analysis of the global markets for large mining

excavators/loaders and haul trucks plots the path forward

with respect to the industrys expected equipment requirements

and attendant shipments through 2020.

All historical data contained in the report are derived

from Parker Bays Mobile Mining Equipment Database, which

identifi es machines by individual mine in more than 100

countries.

Source: The Parker Bay Company.

Source: The Parker Bay Company.

According to the report, during a ten-year period up to 2014,

global equipment manufacturers delivered 6,400 large excavators

(20-mt-plus payload) and nearly 31,000 large trucks

(100-mt-plus payload) with an installed value of nearly $80 billion.

While most of this new capacity was required to fuel the

growth in mineral output, it became clear that by 2013, more mine

capacity had been added than was required by underlying

mineral requirements. The escalating oversupply, combined with

slowing demand, initiated the downward spiral in mineral prices

that continued through year-end 2015. This in turn compelled

companies to close many mines, curtail output at others, and

drastically cut capital expenditures including those allocated for

the equipment covered by the report.

Parker Bays analysis examines the factors now impeding

a recovery and those that will eventually spur a resumption of

growth for these machinery markets. Chief among these factors

are: the excess capacity at minesincluding more than

4,000 machines parked and available for resale and redeployment

when demand warrants it; the eventual requirement to replace

large numbers of the 9,000-plus excavators/loaders and

40,000-plus trucks now in service; and continued growth in

mineral demand in spite of currently depressed prices.

Among Parker Bays key conclusions:

Very slow growth in mineral production through 2020 will

warrant increases in installed machine capacity of less

than 1.5% per year through 2020, compared with annual

increases of 7%-10% per year during the past decade.

The current overhang of surplus machines will reduce nearterm

demand for new machines by as much as one-third

during 2016 and will continue to reduce new machine requirements

through 2018.

Replacement requirements will be the chief driver in

the recovery that will begin in 2017. Despite efforts to extend

equipment service life and reduce the need for investment

in replacements, mines will eventually have to

retire certain machines as they begin to require increased

maintenance and repair and become simply uneconomical

to continue working.

Parker Bay estimates nearly 2,500 excavators/loaders

and 12,000 trucks will reach this stage during 2015-

2020. As a result, a substantial majority of all machines

shipped during this time will be required to simply maintain

the existing fleet.

The result of these combined factors will be an equipment

market that continues at current depressed levels through 2016

and begins recovering in 2017. This recovery will escalate

during 2018-2020 as these markets have in past growth cycles.

But the slow growth in mineral demand will dampen this next

cycle to the extent that projected 2020 shipments will still be

as much as 25% below the 2012 peak.

As featured in Womp 2016 Vol 04 - www.womp-int.com