Source: S&P Capital IQ, PwC Analysis.

PwC Reports Near-record 2011 Mining M&A—Even More in 2012

"Not at all the kinds of behaviors expected in a cyclical downturn," PwC commented.

The report revisits 2011 trends: who was buying and selling, what resources were sought out, what drove deal premiums, and, of increasing importance, what the differences were in buying behaviors between developed and growth market buyers.

Looking ahead to 2012, PwC anticipates a record year of mining M&A, primarily driven by cash-rich seniors and intermediates hungry for projects. 2012, however, is unlikely to be "more of the same," PwC said. A variety of financial funds and vertically integrated buyers, such as steel mills, are likely be active, a state of affairs that should bode well for deal values. PwC also expects that Africa will increasingly become a more viable M&A geography, with growth-market buyers in particular driving substantial acquisition volumes.

In 2012, PwC expects public companies in the West will increasingly find themselves in an unfamiliar world. Many miners have not yet mastered frontier markets, the report states; and shifting centers of gravity from west to east will increasingly challenge the traditional economics behind mining M&A deals, forcing Western boards and shareholders to reconsider the manners in which the balances of risk and reward are weighed.

The value of announced mining M&A transactions with disclosed values reached $149 billion in 2011, 33% higher than in 2010 and only 2% short of the peak value in 2006. Seven deals worth more than the U.S. dollar equivalent of $5 billion were announced, with total values in this segment registering increases of 145% and 490% over 2010 and 2009, respectively. Deals in the $1 billion to $5 billion segment included 23 transactions worth $43 billion. Measured by value, this represented a 14% increase over the prior year and was double the 2009 tally.

At the opposite end of the spectrum, the junior sphere also had a blockbuster year. In the less than $100 million segment, 1,355 deals worth $36 billion were announced, both all-time records. Deals in the $100 million to $1 billion range experienced a moderate year-over-year contraction in aggregate value, as 25 deals worth $17 billion were announced, a decrease of 6% from 2010.

Buyers from Canada, Australia and the United States continued to dominate the mining M&A market in 2011, but buyers from Asia, Latin America and Russia were increasingly active. PwC's analysis shows that, with the exception of a small number of outliers, buyers in both the developed and growth worlds were biased toward transacting within their own regions. Very little "cross-pollination" was observed between the two worlds. Buyers from India were a notable exception to this trend.

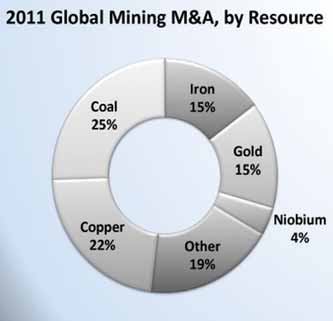

When analyzed by commodity, gold, coal, copper, iron ore and niobium represented 81% of the aggregate target values for mining M&A in 2011. The PwC report includes a tabulation of the top 20 mining deals during the year, and separate tabulations of the top five deals in each of the gold, coal, copper and iron ore sectors.

A special feature in the report focuses on copper, which enjoyed a 300% increase in price per pound between 2000 and 2010 but which experienced a 21% drop in 2011. That decline did not dampen copper M&A activity, as miners continued to point to strong long-term copper market fundamentals. Even with the price down 21% in 2011, the average spot price for copper throughout the year was $4.00/lb, 17% higher than the 2010 average spot price, 24% higher than the spot price during 2007, and 386% higher than the average spot price in 2000.

Overall, PwC identified acquisitions of copper projects in 29 countries on six continents. Of these, 53%, measured by the number of deals, were in the traditional copper belts of Canada, Chile and Australia. Copper projects in Canada were the most sought after, accounting for more than 33% of all targets. Despite this bias, some buyers also sought out targets in other promising geographies, including Mongolia, China, Democratic Republic of the Congo, Zambia and Namibia.

The PwC report also includes a special feature spotlighting gold M&A activity and a case study of Canadian iron ore development company Century Iron Mines Corp.

The report is available as a free download at www.pwc.com/ca/miningdeals.