Avalon Rare Metals’ Nechalacho project near Thor Lake, Northwest Territories, Canada, is emerging as one of the largest undeveloped rare-earth resources in the

Avalon Rare Metals’ Nechalacho project near Thor Lake, Northwest Territories, Canada, is emerging as one of the largest undeveloped rare-earth resources in the

world. The

Ontario-based company's prefeasibility study, completed earlier this year, estimated it would require an investment of roughly C$900 million to start up a

10,000-mt/y

underground mining operation there, producing rare-earth oxides plus zirconium, niobium and tantalum. An Avalon geologist is shown here examining

Nechalacho drill core

samples. (Photo courtesy Avalon Rare Metals).

This scenario provides a close analogy

with the rare-earths market. Having effectively

run competitive producers off the

block 10 years or so ago, China has established

a level of domination in rare-earths

production that is unsurpassed in other

mineral commodities. Consumers in the

U.S., Japan, Europe and elsewhere have

become wholly dependent on imports from

China, a position The New York Times highlighted

in an article in September 2009.

According to the U.S.-based analyst,

John Kaiser, the trigger for the sudden

media awakening to this situation arose the

previous month with the publication by the

Chinese Ministry of Industry and Information

Technology of a draft report on the

country’s policy for its rare earths industry

up to 2015. The inclusion of plans to tighten

controls on the supply of rare-earth

oxides and downstream products from

China, and possibility of an export ban on

specific rare-earth metals, provoked industry-

wide jitters over the security of supply.

With China later apparently confirming

cuts in export quotas, the situation was

exacerbated in October this year by the

diplomatic spat between China and Japan

over the sovereignty of certain islands that

lie between the two countries, with

Chinese exporters withholding supplies of

specific rare earths. Cerium, a key ingredient

in abrasives used in the production of

polished glass components for flat-panel

televisions and hard-disc drives, was one of

the metals affected.

Chinese officials attempted to assuage

U.S. and Japanese fears over its rare-earth export plans at the ASEAN summit in late

October, with the country’s Foreign

Minister Yang Jiechi assuring U.S.

Secretary of State Hillary Clinton China

“will not use rare earths as a diplomatic,

political or economic tool in dealing with

other countries.” Nonetheless, while

accepting this statement, Clinton pointed

out the Chinese export restrictions are “a

wake-up call” for the world to seek additional

sources of rare earths.

So, how did the world’s rare-earth users

get into this situation in the first place, and

what is being done to develop alternative

sources of supply now that China seems

almost certain to cut back on its exports?

Not, the Chinese say, from the perspective

of wishing to exercise an increasing level of

control but because of the burgeoning

demands from their own domestic industry.

China’s Rise to Dominance

From initial interest in rare earths for limited

military purposes, the market expanded

slowly during the third quarter of the 20th

century. By 1987, major users included the

glass and ceramics industries, the production

of catalysts for oil refining, and in metallurgy

as alloying materials. At that time,

less than 5% was being used in electronics

and the production of high-intensity magnets.

Twenty years on, and the picture is

markedly different, according to the U.S.

Geological Survey: while metallurgical

applications and alloys still take up nearly

one-third of demand, rare-earths usage in

electronics has risen to a similar proportion.

On the face of it, national governments in

the market-economy countries seem to have

been remarkably complacent during the

1990s and 2000s, as China became increasingly

dominant within the international

rare-earths market. Since Chinese producers

could supply what was needed at lower costs

than established producers in the U.S. and

elsewhere, they effectively drove their competitors

out of business. From the world’s

leading producer, based on the Mountain

Pass deposit in California, the U.S. joined

the ranks of those dependent on imports to

satisfy domestic industrial demand.

China has two principal sources of rareearth

metals: by-product output from the

Bayan Obo iron ore mine in Inner

Mongolia, and low-grade ion-absorption

clay deposits in the provinces of Jiangxi,

Guangdong, Hunan, Guangxi and Fujian in

southern China. Commercially, the two are

complementary, since Bayan Obo’s output

is principally of ‘light’ rare earths, while the

clays contain a higher proportion of ‘heavy’

elements. What the two have in common is

their low cost of production, at least on an

historical basis, although recent Chinese

awakening to environmental issues and the

legacies of past mining practices appear to

be whittling away at that advantage. Other

Chinese production comes from deposits in

Sichuan and Shangdong provinces.

Discovered in 1927, Bayan Obo was

initially considered to be an iron ore deposit.

However, nine years later its rareearth

potential was recognized, with niobium

being added to its list of resources in

the late 1950s. According to Mindat, the

deposit contains 470 million mt of iron-ore

reserves, plus some 40 million mt of mineralization

grading 3.5%-4% rare earths, 1

million mt of Nb2O5 and 130 million mt of

fluorite. Stratiform and lenticular orebodies

occur within quartzite, slate, limestone and

dolomite host rocks.

Worldwide, the development of new

uses for rare-earth metals has traditionally mirrored their availability, with the U.S.

taking the lead in this respect once

Mountain Pass came on stream in 1952.

Neither was China an exception here, with

national scientific and industrial development

programs that were put in place during

the 1980s and 1990s including studies

on new uses for the country’s extensive

rare-earth resources.

Thus, not only has China been able to

supply virtually all of the rare-earths needed

by the rest of the world, but it has also

developed its own technical expertise in

their use. As a result, domestic demand

has surged, not only to supply export-orientated

industries such as electronics, but

also to satisfy demand from newly emerging

technologies such as wind turbines and

hybrid cars. With international pressure on

China to reduce its carbon emissions, and

realization gained during preparations for

the 2008 Olympic Games, these have

taken on new importance within the

national economy.

Annual Output Trends

and Reserves

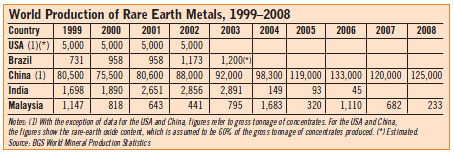

According to statistics gathered by the

British Geological Survey, worldwide production

of rare earths has been rising

steadily over the past 10 years. The data

shown in the table on p. 50 clearly illustrate

China’s increasing dominance in the

world market, with a 50% increase in output

over the period from 1999 to 2008.

The BGS notes, however, its data set is not

complete, and a number of other countries—

including Indonesia, Kazakhstan,

North Korea, South Korea, Kyrgyzstan,

Mozambique, Nigeria, Russia and

Vietnam—are believed to have limited

rare-earth production.

In a presentation to this year’s SME

conference in Phoenix, the USGS’s rareearths

expert, James Hedrick, cited a figure

of 124,000 mt of contained rare-earth

oxide production worldwide in 2008, of

which China had a 97% share, India

2.2%, Brazil 0.5% and Malaysia 0.3%. He

also presented a graph of production

trends since the early 1950s, which clearly

indicates the accelerating trend over the

subsequent period as more uses were

found for rare earths, and demand rose

accordingly.

In terms of world reserves, the USGS

reported a total of 99 million mt in its most

recent Mineral Commodity Survey publication,

although noting the resource base is

probably much greater. Bastnaesite deposits in China and the United States hold

the greater proportion of current reserves,

while the bulk of the remainder is contained

in monazite deposits in Australia,

Brazil, China, India, Malaysia, South

Africa, Sri Lanka, Thailand and the United

States. A breakdown of known reserves is

shown below.

The risk of Chinese supplies being cut,

either in part or in total, has already led

some governments to consider introducing

national rare-earth stockpiles. At the beginning

of October, Japan’s Foreign Minister

Akihiro Ohata stated publicly that a stockpile

was then under consideration as a

buffer against future supply interruptions,

with the country’s trade ministry studying

which specific rare earths should be

included.

Japan’s lead was swiftly followed by

South Korea, which has been reported to

be planning to invest $15 million in building

a 1,200-mt rare-earth stockpile by

2016.

In the U.S., meanwhile, Congress

already has the issue on its agenda. In

March, Rep. Mike Coffman (R-Colorado)

introduced a bill that included a requirement

for the Department of Defense to create

a stockpile of rare earths considered

essential for national security. And, in a

separate move, the government has been

carrying out an investigation into whether

China has been cutting back on its exports

to the U.S. as well as to Japan. In October,

a spokesperson for the U.S. Trade

Representative’s office was reported as

saying, “We’re seeking more information...

into whether China’s actions and

policies are consistent with World Trade

Organization rules.”

However, it is not just the consuming

countries looking at the possibility of stockpiles,

since Baotou Steel Rare-Earth, operator

of Bayan Obo, is believed to be working

on its own inventory store. With its output of around 55,000 mt this year somewhat

greater than the tonnage it is being

allowed to export, the surplus could well

end up there, with the company having

confirmed it had been given permission to

build a 200,000-mt-capacity storage facility

at Baotou.

To cite some examples, yttrium, terbium

and europium oxides are used in the

red, blue and green phosphor coatings for

LCD and plasma TV screens, and computer

monitors. They also find uses in lowenergy

light bulbs. Wind turbine generators

need neodymium and other rare-earth

magnets, while neo-magnets also help to

cut the weight of vehicles, so making them

more energy-efficient. Other everyday

applications include mobile phones and

computer hard drives, while the defense

industry uses rare earths for things as

diverse as jet engines, radar, night-vision

systems and missile guidance, as well as

more general electronics.

In a presentation made to the Rare

Metals Summit III in October, the

Australian producer Lynas Corp. gave an

overview of current and projected demand

trends for rare earths. The principal enduses

at the moment include magnets (26%

of total demand or some 35,000 mt/y of

rare earths), the company said, catalysts

for hydrocarbon cracking (21,300 mt), polishing

powders (19,100 mt) and battery

alloys (18,600 mt). Other end-uses

encompass metallurgical alloys, glass additives,

auto catalysts and phosphors.

By 2014, according to Lynas’s estimations,

total demand will have grown from

136,100 mt to 190,100 mt, with the

main growth drivers being battery alloys

and magnets, and rare-earth use in polishing

powders also increasing strongly. In

fact, the only area of use predicted not to

see any growth is in the most traditional of

rare-earth applications: as a colorant in

glass-making.

Applications for rare-earth products encompass a wide range of technological sectors. Clockwise from left: military uses extend beyond phosphors for monitor

screens; mobile

telecommunications has provided substantial market growth; they’re needed in the growing hybrid and electric-vehicle sector; as well as in

“green” market initiatives

illustrated here by an offshore wind-turbine farm. (Photos courtesy of BAE Systems, Nokia, Toyoto and E.On UK, respectively).

Construction work in progress on the flotation circuit building at Lynas Corp.s Mount Weld rare earths project in Australia.

United States Industry

Developments...

The threats—real or perceived—from

China about future rare-earth supplies have

certainly spurred interest across the globe

in developing alternative sources. In the

United States, Molycorp Minerals has been

working toward reopening Mountain Pass

in California, while a more recent arrival,

Wings Iron Ore, recently finalized an agreement

with Glencore over reopening the Pea

Ridge mine in Missouri. In Canada, Avalon

Rare Metals is evaluating its Nechalacho

prospect, Great Western Minerals has its

Steenkampskraal project in South Africa,

while in Australia, Lynas Corp. is pressing

ahead at Mount Weld while Arafura

Resources is working at its Nolans tenement.

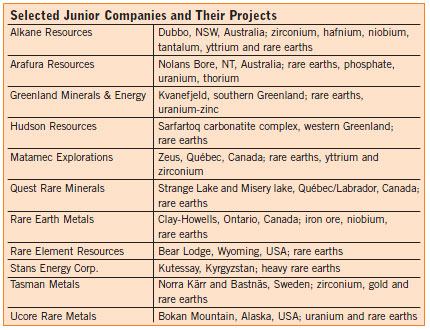

Analyst John Kaiser points out that

other juniors involved in the hunt include

Alkane Resources, Greenland Minerals & Energy, Hudson Resources, Matamec

Explorations, Quest Rare Minerals, Rare

Earth Metals, Rare Element Resources,

Stans Energy Corp., Tasman Metals and

Ucore Rare Metals, all of which are listed

in stock exchanges in Canada or Australia.

From the U.S. perspective, the reopening

of Mountain Pass would be a

major landmark in terms of resuming a

level of self-sufficiency in national rareearths

requirements. Opened in 1952 by

the Molybdenum Corp. of America, by the

mid-1960s the operation had an annual

capacity of 10,900 mt of rare-earth concentrates.

The renamed Molycorp was subsequently

bought out by the oil company,

Unocal, which in turn merged with Chevron

in 2005. In 1998, however, operations at

the processing facility were curtailed as a

result of environmental concerns over thorium

and radium emissions from plant

wastewater, with mining ending in 2002.

The current owner, Molycorp Minerals,

bought the operation and its facilities

from Chevron in 2008, since when it has

been running pilot plant-scale operations

on stockpiled feed material. In July of this

year, the company raised $379 million in

an IPO, with the proceeds being used

toward the estimated $511 million cost of

renovating the existing facilities and resuming

mining in 2012. Its stated aim, under

its ‘mine-to-magnets’ strategy, is to become

one of the world’s most highly integrated

producers of rare-earth products, including

oxides, metals, alloys and magnets.

Molycorp Minerals is projecting an output

of 19,050 mt/y of rare-earth oxides

once Mountain Pass is back to full production.

In the meantime, it has entered into a

number of agreements with other companies

over the development of future downstream

activities, including the production

of high-strength neodymium-iron-boron

magnets. Current revenue is being generated

through the sale of lanthanum concentrates

to consumers in the catalyst industry.

In its IPO prospectus, the company

cited proven reserves of some 40,000 mt

of rare-earth oxides at an average grade of

9.38%, plus 962,000 mt of oxides in

probable reserves at a grade of 8.2%. This,

it said, would give a mine life of over 30

years, with the possibility of increasing output

to 40,000 mt/y if the market exists.

In Missouri, meanwhile, privately

owned Wings Iron Ore acquired the Pea

Ridge property in 2001. Originally owned

by Bethlehem Steel and St Joe through

Meramec Mining Co., Pea Ridge produced

over 27 mt of iron ore products between

1964 and its closure in 2001. Its acquisition

by Upland Wings led to a small-scale

resumption of production in 2006, based

on a tailings-retreatment operation.

Wings has budgeted US$390 million in

pre-production costs to bring the mine

back into operation at a rate of 3.6 million

mt/y of iron-ore products, based on a 136-

million-mt magnetite resource. However,

the Pea Ridge orebody also contains rareearths,

both in apatite (phosphate rock)

within the main ore and also within separate,

high-grade breccia pipes. Old tailings

also contain recoverable rare earths. More

importantly, the company states, Pea

Ridge has a higher proportion of heavy rare

earths (samarium, europium, gadolinium,

terbium and yttrium) than any of the other

major rare-earth sources, including

Mountain Pass, Bayan Obo and Mount

Weld in Western Australia.

In October, Wings signed a marketing

deal with Glencore over its future rare-earth

output. A feasibility study is scheduled to

begin by mid-December, with completion

due in the second half of 2011, although

development will depend on the partners

being able to secure competitive funding.

Assuming that this is achieved, a restart to

mining is penciled in for 2012 with a

ramp-up to full production the following

year, including 42,000 mt/y of apatite and

1,900 mt/y of rare-earth oxides.

...and Overseas

Situated within one of the main mining districts

in Western Australia, Lynas Corp.’s

Mount Weld project is based on a carbonatite-

hosted resource that contains niobium

and tantalum as well as rare earths. The

company bought the property in 2001 from

Anaconda Nickel (now Minara Resources)

for A$5 million. Trial mining in 2007 and

2008 produced 770,000 mt of ore grading

15.4% rare-earth oxides, but construction

at the mine site and at Lynas’s advanced

minerals plant in Malaysia was suspended

in early 2009 when the company lost its

source of funding. An equity issue in

November last year raised A$450 million,

which allowed it to resume work, with concentrator

construction scheduled for completion

this month. Initial capacity will be

33,000 mt/y of concentrate grading 40%

rare-earth oxides, which will be shipped to

Malaysia for further processing into 11,000

mt/y of rare-earth oxide products.

The company recently revised its

resource estimate for Mount Weld upward

to a total of 17.49 million mt grading

8.1% total rare-earth oxides, or 7.9% lanthanides

(not including yttrium). It has

divided its resource into two distinct zones,

the 9.88-million-mt Central Lanthanide

Deposit, which grades 10.7% total rare

earths, and the 7.62-million-mt Duncan

deposit which, although it grades 4.8%,

contains a higher proportion of heavy rareearth

metals.

In 2007, Lynas paid US$4 million for

the Kangankunde carbonatite-hosted rare-earth resource in Malawi. At the time, the

deposit represented an inferred resource of

107,000 mt of rare-earth oxides which,

the company noted, could form the basis

for an output of at least 5,000 mt/y of rareearth

oxides for processing at its Malaysian

refinery.

In Canada’s Northwest Territories,

Avalon Rare Metals is just the latest in a

sequence of companies that has included

Highwood Resources, Placer Dome, Hecla

and Navigator Exploration Corp. to have

worked on evaluating the mineralization at

Thor Lake. Resources at the focus of current

attention, the Nechalacho zone, now

total 14.48 million mt indicated at 1.82%

total rare-earth oxides plus 175.5 million

mt inferred at 1.43%, the company stated

in June.

As well being relatively enriched in

heavy rare earths, the Nechalacho deposit

contains tantalum, niobium, gallium and

zirconium mineralization. A prefeasibility

study completed earlier this year indicated

capex costs of virtually C$900 million for

an 18-year underground mining operation

with an output of around 10,000 mt/y of

rare-earth oxides, plus zirconium, niobium

and tantalum. In September, Avalon raised

C$30 million in a share sale, and a month

later received a scoping study for a 25,000

mt/y rare-earth separation plant which, the

study suggested, would carry a near-

C$350 million price tag.

Canadian-domiciled company Great

Western Minerals has a number of rareearth

exploration projects on the go in

North America, plus an option over the

rehabilitation of the old Steenkampskraal

mine in northwestern Cape Province in

South Africa. The mine was operated by an

Anglo American subsidiary between 1952

and 1963 principally as a thorium producer,

with the current owner, South Africa’s

Rareco, acquiring it in 1989.

The deposit consists of a tabular monazite-

rich orebody hosted in pegmatites,

with accessory copper, lead, zircon and

ilmenite. The monazite contains an average

in-situ grade of 17% total rare-earth

oxides, making Steenkampskraal highestgrade

rare-earth deposit in the world, the

company claims.

Based on historical data, current

resources total just under 30,000 mt of

rare-earth oxides. The company began a

feasibility study on the project in June this

year, and subsequently raised C$35 million

in a share offering as well as taking a

21% stake in Rareco.

Will the Future be Secure?

There is no doubt that after a considerable

period of complacency, the Western

World has finally woken up to the potential

consequences of China no longer

being able to supply all of its rare-earth

requirements. There has been a marked

increase in exploration activity, with

known prospects being revisited and new

ones prospected. Not surprisingly, there

has been a fair amount of media hype

that has helped spur wider interest in the

topic on the one hand, and risks creating

a ‘rare-earth bubble’ on the other.

Some hard facts remain undisputed,

however. Hard drives and wind turbines

have a mutual need for high-strength

magnets, as do the increasing numbers

of motors found in modern cars.

Automotive technology is also changing

focus, with hybrids increasing their market

share and conventional cars needing

more effective exhaust catalysts. Nickelmetal

hydride batteries are finding more

and more applications, while better

hydrogen-storage capabilities will be

needed as alternative energy-carrier

options become more widely available.

All of these uses have one thing in common:

rare earths.

Rare Earths: Not All That Rare, and

They’re Metals, to Boot

The term ‘rare earths’ is invariably described as misleading, since the

elements themselves are neither particularly rare and are all metallic.

The expression usually covers the 15 elements in the lanthanide

series in the periodic table, plus yttrium and scandium. Although

these are not in the same periodic group, they occur with the lanthanides

in rare-earth deposits, and have comparable properties.

Rare-earth elements are classified as being ‘light’ or ‘heavy’,

the difference stemming from ionic compaction within the atom.

Light rare earths include the lanthanides from lanthanum (element

57 in the periodic table) up to europium (63), while the

heavy rare earths are those from gadolinium (64) to lutetium (71),

plus yttrium.

The principal rare-earth ores, the minerals bastnaesite and

monazite, have formed the basis for historical production, with

minor contributions from deposits containing xenotime and

loparite. A significant proportion of Chinese rare-earth production

is sourced from ion absorption clays, which themselves appear to

have been derived from the deep weathering of source rocks containing

xenotime.

Until the discovery of carbonatite-hosted rare-earth deposits,

such as Mountain Pass, all rare-earth production came from monazite,

with beach-sand operations in India and Brazil the leading

producers. A phosphate mineral, monazite is known to exist in at

least four forms, depending on whether Ce, La, Nd or Pr is the

principal rare-earth constituent. Its main drawback is its thorium

content, with concerns over the potential radioactivity of tailings

having effectively rendered it unacceptable as a commercial ore in

most parts of the world. Minor monazite production resumed in

Brazil in 2004, according to British Geological Survey data, while

Indian production has tailed off completely. Malaysian monazite

production comes as a by-product of alluvial tin mining.

A carbonate-fluoride mineral, bastnaesite also has more than

one composition, with Ce, La or Y forming the main rare-earth

component. Typically hosted in carbonatite deposits, this is now

the main source of world production. It is also present with monazite

at Bayan Obo in China, although this is not a carbonatitetype

deposit. Bastnaesite won from Mountain Pass supplied the

U.S. market with rare earths for most of the last 60 years, with

small-scale production having resumed in 2008 after a six-year

hiatus. Bastnaesite is typically richer in the ‘light’ rare-earth metals

than is monazite.

Of the other source minerals, xenotime is also a rare-earth

phosphate in which yttrium is the major component; a number of

heavy rare earth elements can replace some of the yttrium in the

atomic structure, as can thorium and uranium. Virtually the only

source of xenotime is now as a tin-mining by-product in Malaysia.

Individual rare-earth elements can vary widely in their relative

natural abundance, ranging from cerium, the most abundant, to

promethium which, being subject to radioactive decay, is virtually

unknown in ore deposits. One interesting feature of the lathanides

is that the Oddo-Harkins rule applies to their occurrence in nature,

in that the odd-numbered elements occur less extensively than the

even-numbered ones.

In terms of physical properties, there is a general increase in

rare-earth metal hardness, density and melting point from cerium

to lutetium. There is also widespread readiness for the metals to

oxidize at relatively low temperatures, with ignition in air in the

temperature range 150°C–180°C. |

As featured in Womp 2010 Vol 10 - www.womp-int.com