Following a year in which mineral exploration

budgets plummeted, mostly from

financial strain in the junior company sector,

attendance at the 2010 Prospectors &

Developers Association of Canada (PDAC)

convention and trade show exhibited few

signs of waning interest in exploration

issues. According to PDAC, total attendance

at this year’s annual event was a

record 21,660, surpassing the 2008 convention’s

20,168 attendees, with roughly

1,000 companies participating in either

the trade show or investors exchange.

The show’s robust attendance figures

highlighted an optimistic mood pervading

the industry—not the giddy attitude of the

boom days preceding the 2008 bust, but

more a sense of relief from unfulfilled

expectations that the industry was facing a

long, difficult and uncertain recovery.

Those fears mostly vaporized as 2009 progressed:

by March, commodity prices had

noticeably strengthened, driven by Chinese

demand, and precious metals rebounded.

From late 2008 to late 2009, for example,

gold was up more than 25%, silver more

than 57% and platinum almost 63%.

To be sure, 2009 wasn’t a banner year for

exploration. Metals Economics Group, a

Halifax, Nova Scotia-based firm which tracks

exploration statistics worldwide, reported

planned nonferrous exploration budgets of

the 1,846 companies participating in its

annual survey on corporate exploration

strategies totaled $7.32 billion for 2009—

down from a record $12.6 billion in 2008,

marking the largest one-year decline in the

past two decades. However, despite the deep

cuts to exploration plans, the industry’s

2009 nonferrous exploration budget total

remained well above levels seen prior to

2006, according to MEG. Junior-company

exploration spending fell by more than half in

2009 compared with the previous year, followed

to a lesser degree by intermediate producers—

the result being that exploration

budgets among the major producers stood

atop the heap for the first time since being

overshadowed by juniors in 2004.

The financial blow dealt by the global

economic downturn caused widespread

damage among the juniors, dropping market

capitalization for both the TSX-V mining

sector and the entire TSX-V by more

than half from 2008 levels. However, MEG

attributed the drop in junior-company

exploration spending to a sector-wide cutback

by companies just trying to survive

the slump, citing its data which indicate

the number of juniors actively exploring fell

by only 6% from 2008 to 2009.

A February 25, 2010, report issued by

PriceWaterhouseCoopers Canada detailed

the losses incurred by junior companies

following the economic slump. “In the 12

months ending June 30, 2009, the global

financial crisis eroded the share prices of

most junior mining companies and made it

nearly impossible for many of them to raise

money to finance their projects,” wrote

Paul Murphy, partner and mining industry

leader for PwC. “While some investors were

prepared to take a chance on production

and development companies, exploration

companies, or any company perceived to

carry a higher investment risk, were left out

in the cold.”

As the top 100 TSX-V companies tried to

conserve cash, exploration spending

declined. The top 100 group wrote down a

total of $644 million on mineral properties

and exploration as projects were either abandoned

or put on hold. Stock-based compensation

fell in tandem with share prices and

was 30% lower than the prior year.

Smaller mining companies merged in

order to survive, resulting in a 129%

increase in acquisitions by exploration

companies in the top 100 in 2009.

The PwC report pointed out that cash

available to the junior mining sector dried

up in 2008 and financing became even

more challenging for the top 100 in the

first half of 2009. For the year ended June

30, cash provided by financing activities

(both debt and equity) dropped 21% to

$1.5 billion. Expenses also declined as

companies sought ways to economize.

Of the top 100 companies in 2008, the

PwC report stated that only 48 remained in

the 2009 top 100 list. Most of the remainder

dropped off the list as their market capitalizations

fell, while eight—five of them

gold companies—graduated to the TSX and

another seven were acquired. The 100th

company on the 2009 list had a market

capitalization of $25.7 million in 2009,

compared with $72 million in 2008,

reflecting the serious deterioration in market

conditions for the junior mining sector.

The struggle to survive led to a spike in

the number of mining M&A deals involving

junior companies in 2009. On March 1,

PwC issued a press release noting “the

number of small deals (below US$250

million) was significantly above the prior

three years, with a total of 1,859 deals.

This trend was driven by consolidation of

smaller players and deals driven out of

necessity for survival rather than opportunistic

or strategic growth ambitions.”

Questioning Exploration

Efficiency

The sudden shrinkage of industry exploration

budgets renewed debate over some

broad, ongoing issues: Are companies—

and investors—getting the best bang for a

buck out of their exploration programs?

Overall, how good of a job is the industry

doing in finding new deposits and replenishing

reserves? How can exploration performance,

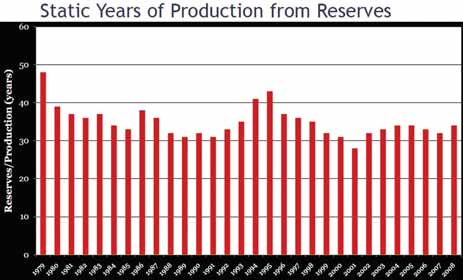

One measure of exploration effectiveness is the ratio of reserves to production for any given year, according to

One measure of exploration effectiveness is the ratio of reserves to production for any given year, according to

Michael Doggett, president and COO of HanOcci Mining Advisors. Speaking at PDAC 2010, Doggett presented this

chart to illustrate that the copper industry, for example, despite doubling annual production during the past 30

years, has steadily maintained a reserve base of more than 30 years of production. Source, Doggett, PDAC 2010,

“Measuring Exploration Effectiveness and Efficiency: Do we need to do better? Can we improve?”.

During the period 1979–2008, continued

Doggett, copper reserves in 1979 were

350 million metric tons (mt); in the following

30 years the industry produced 322

million mt, and at the end of the period

reserves were reported as 550 million mt. Exploration during that span resulted in a

net addition of 522 million mt of copper.

To determine the reserve replacement

ratio, he explained, divide net reserve additions

by production:

• For 1979-2008 = 522/322 = 1.6

• Similarly, the reserve replacement ratio for

• 20 years (1989-2008) = 1.9

• 10 years (1999-2008) = 2.0

“We have consistently added reserves

at a rate far exceeding overall production.

Does this look like an industry with a discovery

problem?” said Doggett.

Continuing in the same vein, he said

another simple measure of exploration

effectiveness is the ratio of reserves to production

for any given year. This metric represents

the number of years of output supported

by the current year’s reserves, assuming

no growth in annual output or reserves.

If this metric does not decline over time,

then exploration is effective in both replacing

reserves and sustaining growth trends.

“In spite of doubling annual production

during the past 30 years, we have been

able to maintain a base of more than 30

years of production at current rates moving

forward. Does this look like an industry

with a discovery problem?” Doggett said.

“As an industry we have been highly

effective in replacing reserves through

exploration, but this measure does not say

anything about what it costs to be highly

effective. To do that we need to factor in

the amount of money spent on exploration,”

he said.

During 1979–2008, the global copper

industry spent approximately $22.5 billion

on exploration; over the past 20 years, it

spent $17.7 billion, and over the past 10

years, $10.3 billion.

“We can measure exploration efficiency

by considering how much it cost to add

reserves over time,” he said. “Consider an

efficiency of exploration metric whereby z =

net reserve additions, a = cost of making

additions (exploration expenditure), with

a/z = cost per unit of adding reserves. Thus,

the cost of adding a unit of copper reserves

from 1979-2008 was: $22,540 M / 522

million mt = $43.20/mt ($0.02/lb).”

This calculation shows that over 30

years ($0.020), 20 years ($0.016) and 10

years ($0.016) the industry, in terms of

efficiency, has generally been able to consistently

add copper to reserves for two

cents or less per pound of copper—another

indication of exploration efficiency. In

addition, Doggett said the copper industry

has consistently spent 2%–4% of sales

revenue on exploration, in contrast to the

gold sector, which at times spent more

than 12% of sales revenue on exploration

during the same period.

As for the probability that this efficiency

can be sustained in the future, he suggested

that in recent years exploration

effectiveness and efficiency have been

driven by brownfield additions to reserves

in conjunction with major expansions at

the world’s largest copper mines. For

much of the next decade, this will continue

to be the case. Beyond 2020, however,

the ability to increase reserves and annual

output at known mines is at best uncertain.

The underlying resource base is large

but much of these resources are challenged

by political, economic, social and

technological issues.

Long lead times to find and develop new

mines (on average 20 or more years) restricts the conversion of resources to

proven and probable reserves. To meet

anticipated demand for new primary supply

of copper, the industry can only bank on

brownfield success for so long. New discoveries

are essential. Exploration effectiveness

and efficiency will necessarily decrease

when this crossover point is reached.

“Can the industry do better [in exploration]?”

Doggett questioned. “In the face

of the cumulative impact of billions of dollars

of exploration expenditures in the past

few decades, it is completely unrealistic to

think that we will magically get better at

exploration.” There’s no silver bullet or

panacea on the horizon, he suggested, but

to date, advances in technology and the

cumulative base of knowledge gained from

past exploration have been dependable

factors in keeping up with the relentless

forces of depletion.

Gold: Searching for Reserves

Stephen Enders, director and principal

consultant at Renaissance Resource

Partners, Denver, Colorado, USA, and former

senior vice president of worldwide

exploration at Newmont Mining Corp., presented

a less sanguine view of exploration

performance and expectations—at least

’s point of view.

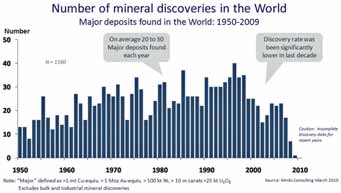

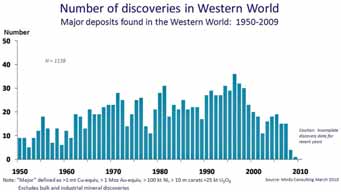

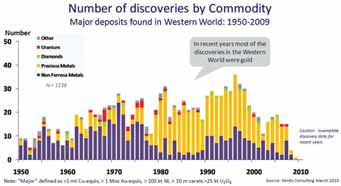

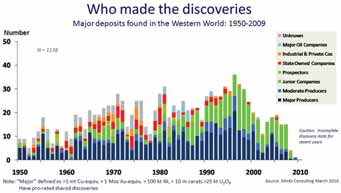

Mineral discovery trends, 1959-2009. Source: Richard Schodde, MinEx Consulting, PDAC 2010, “Global discovery trends 1950-2009: What, where and who found them.”.

Mineral discovery trends, 1959-2009. Source: Richard Schodde, MinEx Consulting, PDAC 2010, “Global discovery trends 1950-2009: What, where and who found them.”.

There’s also a major disconnect in what

major producers want—in terms of exploration

success—and what junior companies

can accomplish, he stated, suggesting

that majors are exploration-phobic and

much prefer to acquire discoveries without

having to spend the time and resources to

conduct their own exploration effort.

Juniors, on the other hand, mainly function

on an extremely short-term financing timeline.

He estimated that only about 30% of

juniors are seriously interested in creating

wealth for others—“the rest are focused on

creating wealth from others.” And, perhaps

50% or more of junior funding “never goes

into the ground. They spend it just keeping

their lights on,” Enders said.

He said the gold business is quite different

from copper—the median gold

deposit size is about 350,000 ounces,

much smaller than typical copper discoveries

and much quicker to deplete. Because

of the difficulty of replacing reserves to

maintain production, he believes that

“from a major’s perspective, [gold] is not a

sustainable business” by itself and that’s

why major gold producers are now focusing

on finding porphyry copper-gold deposits.

Discovery Rate Declines

In the same session, Richard Schodde,

managing director of MinEx Consulting,

Melbourne, Australia, presented results of

a study on global discovery trends from

1950–2009, focusing on how many

deposits were found, what commodities

were involved, where were they found and

who discovered them. The study included

nonferrous metals, precious metals, diamonds,

and uranium but excluded bulk

minerals (coal, iron ore, bauxite) and

industrial minerals such as potash, talc or

phosphate. It also ignored discovery of

satellite deposits feeding into an existing

mill within an established mining camp

(for example, it counted the Ekati diamond

discovery as one world-class discovery, not

20 small discoveries), and limited analysis

to major deposits ( > 1 million mt Cu

equivalent, > 100 kt Ni, > 1 million oz Au,

> 10 million carats, > 25 kt U3O8, etc.). It

also assessed quality of the discoveries

(Tier 1, Tier 2).

The study’s findings, in a nutshell:

• In spite of record exploration expenditures,

the rate of discovery has declined

over the last decade.

° Industry is now finding less than

10–20 major deposits per year.

° Only one to two of these are “worldclass.”

° The gold industry is struggling to replace

the ounces it mines.

• In the last 20 years there has been a steady

shift away from the established countries.

° In the 1980s, Canada, the U.S. and

Australia accounted for over half of

all major discoveries. Now it is less

than 20%.

• Since 1980, the “main game in town”

has been gold.

° Currently 60%–80% of all major

discoveries are gold-related.

° The current hot spots for gold are

Colombia/Ecuador, West Africa and

Central Africa.

° The size and grade of the discoveries

(for gold) is declining.

° Few major lead-zinc, diamond or

uranium deposits have been found

in the last decade.

• Since the 1990s, juniors have played a

significant role in discovery.

° Currently over half of all major discoveries

in the Western World are

made by junior companies and

small producers.

As exploration drilling steadily moves

toward jobs involving deeper deposits in

remote areas, requirements for more powerful

drills, longer-lasting core bits and better

driller accommodations are being met

by industry suppliers.

Boart Longyear’s new SC11 flyable exploration drill rig is designed to be transportable in nine to 11 helicopter

Boart Longyear’s new SC11 flyable exploration drill rig is designed to be transportable in nine to 11 helicopter

lifts,

with the heaviest module weighing 680 kg (1,500 lb).

“The SC11 is built from Boart Longyear’s

proven LM technology and designed for use

in surface applications where access is limited

and drill footprint is a critical consideration,”

said Craig Mayman, global product

manager for capital equipment. “It’s

extremely flexible—conveniently assembling

and disassembling in flyable, compact modules—

and in colder regions, its compact size

enables operation inside a drill shack.”

The SC11 was literally built around the

engine—a John Deere 4045HF485, 4.5-

liter, Tier 3 diesel rated at 172 hp (128

kW)—to take advantage of its high power rating.

The SC11 delivers large-diameter and

deep-hole drilling capacity with a 132-kN

pullback rating and PQ handling capacity.

The rig features a variable-speed motor that

provides low-end torque output of 5,456 Nm

at the head for tri-cone drilling and a 1,230-

rpm speed for diamond drilling. The rig also

has efficient hydraulics to easily make or

break rod joints and transport rods safely.

Hydraulic actuators control the rig’s rod

handler, providing movement in three

dimensions. The rod handler has proximity

sensors to protect the operator by preventing

rod drops when operators are nearby. A

laser beam system positioned between the

helper and rod-handler control panel stops

movement when drillers enter the operating

area. Once the beam is interrupted, the

rod handler immediately stops and can

only be restarted when the driller resets it.

The rig uses Boart Longyear’s Nitro

Chuck with gas-charged springs that actuate

the jaws holding the rods to provide failsafe operation. Control panel levers also feature

lift-to-shift rotation and feed actuation

that protect against accidental actuation.

The SC11 has been designed to break

down into flyable modules, with the heaviest

lift weighing 680 kg (1,500 lb), and

depending on drill configuration, it is transportable

in nine or 11 (with skid base and

rod handler) lifts. Lifting points are positioned

at the module’s center of gravity to

provide a balanced load, while quick-connect

hydraulic couplings speed assembly

and disassembly and prevent oil spills. All

modules utilize visible guides to help operators

quickly align and assemble the rig,

speeding up the setup process. Pressed

steel framing with male-female joints help

the modules drop into position and highly

visible jacking and lifting points make

assembly and disassembly safe and easy.

The SC11 is built at Boart Longyear’s

Perth, Western Australia, facilities and

units have been field tested in New

Zealand and Indonesia.

Monika Portman, Boart Longyear’s product

manager for coring products, introduced

two recent developments in the company’s

core-bit lineup. A new XP line of surface-set

bits includes 11 configurations designed to

last up to three times longer than conventional

surface-set bits and eliminate the need

to utilize alternative bits in broken ground.

The company sees the largest market for

these bits in the coal sector.

“Our goal was to redefine the surfaceset

category and set a new benchmark for

productivity in soft and sedimentary applications,”

said Portman. “Early testing of

the new surface-set bits confirms the

strength of the engineering and technology

applied in their development.”

The new Surface Set XP line of bits can provide up to

The new Surface Set XP line of bits can provide up to

three times longer life than conventional surface-set

bits, according to supplier Boart Longyear.

Portman said the bits’ RazerCut face

design further increases productivity by

quickly exposing the impregnated diamonds.

This design, she noted, delivers

“sharp-out-of-the-box” performance, with

exposed cutting surfaces for immediate

drilling capability.

By delivering better cutting and deeper

penetration, the bit’s Ultramatrix design

reduces downtime where the bit is not cutting.

Hard seams often destroy traditional

surface-set bits, forcing operators to pull

the rod string out and change bits if ground

formations vary at depth. The Surface Set

XP bits are claimed to provide a “pushthrough”

capability in hard seams, preventing

unnecessary rod trips and enabling

drillers to keep their string in the ground

longer.

Portman said the company also has

upgraded and expanded its Stage diamond

coring bit product line. The new bits

include engineering upgrades to the

Stage3 waterways, a selection of Stage bits

with an optional new 16-mm crown and an

optional face-discharge feature.

Since its release in 2007, said

Portaman, the Stage3 diamond coring bit

remains the industry’s tallest, with a crown

height of more than 25 mm. Its patented

design is claimed to deliver better penetration

rates, longer active drilling in the hole

and fewer rod trip-outs, increasing shift

capacity and overall meters drilled.

“The new design features an expansion

of our patented window to improve productivity,

a revised window layout to increase

strength and also has our new patent-pending

RazorCut face design. The 16-mm

model includes the upgraded Stage technology

and gives customers more choice

when operating at shallower target depths.”

Upgrades to the Stage design include

windows with rounded corners for greater

durability. The new windows increase

resistance to damage caused by debris in

fractured ground conditions. The windows

also feature a new Twin-Taper design; they

taper inward to create more material on the

window’s inner diameter, increasing material

strength and extending product life. In

addition, the tapered windows produce

high fluid velocity in the inner diameter,

resulting in better flushing of fluids, cuttings

and debris.

Portman said the Stage windows are

now positioned to rotate in the opposite

direction of rod rotation, creating more surface

material which further increases the

strength of the crown and improving performance

in all types of ground conditions.

Excore Bits Enhance Efficiency

Not to be outdone, Atlas Copco also introduced

a line of diamond coring bits during

PDAC, noting that their new Excore bit line

is based on the best features of previously

successful designs, but offers new design

points and matrices to achieve optimized

balance between design and metallurgy.

According to the company, testing of the

bit line before launch was rigorous, with

more than 10,000 m drilled in six different

markets under varying conditions

Atlas Copco’s new Excore bit line is available in three

Atlas Copco’s new Excore bit line is available in three

ranges for efficient drilling in soft to very hard rock.

The Excore bit line is divided into three

ranges:

• For soft to medium hard rock with abrasive

and fractured to competent formations

(Matrix series 1-4);

• For medium hard to hard rock with slightly

abrasive and slightly broken to competent

formations (Matrix series 5-8); and

• For hard to very hard rock with competent

formations (Matrix series 9-10).

Each Excore configuration is available

in various crown designs, including

Extended Channel Flush (ECF) for broken

to competent formations, Jet profile for fast

cutting in competent formations, and Face

Discharge (FD) design for extremely broken

and triple tube applications. Combining

these features with different available

crown heights, from 10–16 mm, according

to the company, providews an Excore bit for

every core drilling application.

Atlas Copco provided several case histories

supporting its performance claims for

the Excore line. At Boliden’s Renströmsgruvan

underground mine, for example,

core drilling at the 850-m level is carried

out by Protek Norr AB, a Swedish drilling

contractor. Recent drilling by Protek Norr

has been in a zone in which normal diamond

drill bit life is roughly 100 m, so

when sinking a 900-m-long hole, the driller

must pull the drill string out of the hole

eight times to change drill bits—adding up

to a big loss of productive drilling time.

Atlas Copco’s sales engineer at the mine

suggested a test of an Excore with a Jet profile.

The first Excore drill bit tested had a

service life of 326 m and the best Excore

bit in the test had a life of 347.5 m.

Overall, testing indicated that the average

life of the Excore drill bits was 324 m, more

than three times that of the bits previously

used by Protek in the same formation.

Similarly, South Africa-based drilling

contractor Drillcorp tested Excore bits during

a five-month contract involving 46

holes totaling 20,000 m of core drilling at

a gold mine west of Johannesburg. By the

halfway point of the contract, the contractor

was managing to drill about 30 m per

shift with an average bit life of 60–70 m

while penetrating fractured, troublesome

ground. The contractor tested an Excore

bit, starting in a hole with 250 m left to

finish; normally, a driller would expect to

change bits at least three more times for

that hole, taking at least 6 hours to run the

rods. However, the Excore bit finished the

hole without need of replacement and was

able to drill another 52 m in the next hole.

The first test bit provided 302 m of life—

four to five times the life the contractor had

achieved with previous bits.

Sandvik’s new, modular drill shack is designed to accommodate its

Sandvik’s new, modular drill shack is designed to accommodate its

DE130

and DE140 drill rigs.

The DE150, introduced in 2009, is

Sandvik’s most powerful exploration rig for

underground exploration. A surface version

of the rig is currently under development,

according to the company, and both versions

share many of the proven components

used by other drill rigs in the DE100

series. In underground applications the

DE150 is equipped with a 110-kW (150-

hp) electric power unit giving a maximum

working pressure of 250 bar (3,645 psi)

and oil flow of 300 l/min (79 gal/min). For

surface application the DE150 will be powered

by a diesel engine. The hydraulic feed

cylinder has a push and pull capacity of 15

mt (147 kN), which is exceptional in relation

to the weight, said Sandvik. Depth

capacity is up to 2,000 m with NQ rods.

The drill unit features a torsion-resistant

steel profile feed boom and a direct

coupled feed cylinder with a feed length of

1,700 mm and maximum feed speed of

0.63 m/s. The feed boom is mounted on a

frame with the tilt cylinder

and mechanical supports.

The mounting frame has

been specifically designed

for quick set-up when fan

drilling, with a full range of

adjustment from vertical

down to vertical up.

Sandvik’s DE150 torque

control enables optimal balancing

of torque and rotation

speed. The control

panel is a pilot-operated

hydraulic system which

gives the operator central

control of all drilling operations

including flush pumps,

wireline hoist and boom tilt.

The system also controls

hydraulic system pressure,

feeding force, hold back

pressure, water pressure and

water flow.

Sandvik also has designed

a drill shack to

accommodate its DE130

and DE140 diamond core

drills. The modular design of

the new Sandvik Drill Shack

makes it suitable for both mobile and stationary

units with quick assembly/pull

down. The drill shack can be packed in

compact units and is suited for helicopter

transportation to remote areas. It can also

be transported in its entirety by tracked

vehicles or mounted on a hook lift frame.

All of the modules needed for operating

the drill shack are built on an identical

platform significantly reducing the number

of components. Modules are fastened to

the floor by T-rail nuts, allowing easy installation,

removal or replacement if needed.

The frame is supported by legs assembled

from the outside and easily removed.

For operator safety, all hydraulics are located

in the frame, keeping the floor free from

hoses and oil leaks. The operator workstation

has a dry, ice-free surface with builtin

floor ducts for heating fluid. The shack's

heating system can be started remotely by

a phone call or by a preset timer. The operator

compartment shares the same heating

system as the rest of the working station,

providing personnel a pleasant working

environment. Sandvik also offers an air

conditioner for applications in sub-tropical

areas. Storage cabinets for coring bits and

tools and a drill pipe stand that can handle

drill pipes up to 6 m are also available

as options.

As featured in Womp 2010 Vol 04 - www.womp-int.com