Gold Producers Must Increase Rate of Reserve Replacement

The group’s average annual cost of producing and replacing gold—incorporating operating costs, capital costs of new mines, sustaining capital costs at existing operations, and reserves replacement costs—more than doubled over the past decade. Although some increased costs were voluntary (mining lower-grade ores and accelerating capital investments for new mines in response to rising prices, for example) and there are signs that costs are beginning to decline, only a tripling of gold prices from the lows of the early 2000s to an average of $872/oz in 2008 has prevented a financial meltdown like that seen in the base metals sector.

In addition to higher costs, exploration programs are encountering increased risks from political and regulatory instability in many developing nations. These countries tend to have inferior infrastructure, less political stability, and uncertain security of tenure—all leading to slower mine development at higher costs. In the current industry-wide gold pipeline (1.7 billion oz of gold in reserves and resources in the 228 advanced-stage nonproducing projects analyzed) 19% is in lower-risk jurisdictions, 57% in medium-risk areas, and 24% in high-risk jurisdictions.

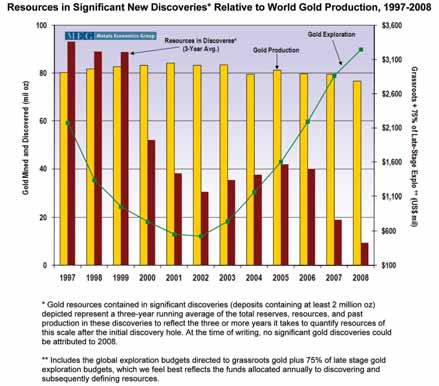

Globally, 62 significant discoveries (each containing at least 2 million oz of gold in total reserves and resources) have been reported so far in the 1997-2007 period. These discoveries contain a potential 377 million oz of gold in anticipated recoverable reserves—less than half of the estimated world gold mine production during the same period. Even anticipating additional reserves from these and smaller discoveries, the industry’s new discovery rate still falls well short of what is needed over the long term. As a group, the major producers developed more than 90% of their exploration- derived reserves by upgrading resources at previously acquired projects and mines or at older discoveries, rather than from recent discoveries.

Increased production by the major gold producers over the past decade has resulted in a greater need to add to reserves in order to maintain a life-of-production that satisfies the long-term views of investors and market analysts. This challenge is further exacerbated by the majors’ larger size requirements for new projects. Based on 2008 production, the major producers need to replace an average of almost 2 million oz/y of reserves, ranging from a high of almost 8 million oz annually for Barrick Gold to about 500,000 oz for those companies at the bottom of the list. Although, as a group, the major producers successfully replaced almost twice their total production over the past 10 years, almost all of these reserves additions were achieved through acquisitions or by upgrading resources at existing projects and mines, and not through finding new significant discoveries.